9. Continuous Probability Distributions

General Terminology and Notation

A continuous random variable is one for which the range (set

of possible values) is an interval (or a collection of intervals) on the real

number line. Continuous variables have to be treated a little differently than

discrete ones, the reason being that

has to be zero for each

has to be zero for each

,

in order to avoid mathematical contradiction. The distribution of a continuous

random variable is called a continuous probability

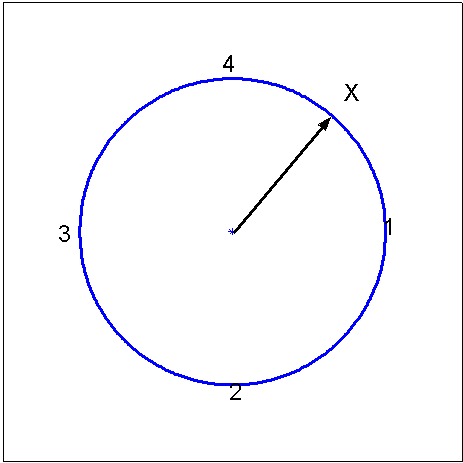

distribution. To illustrate, consider the simple spinning pointer in

Figure

spinner.

,

in order to avoid mathematical contradiction. The distribution of a continuous

random variable is called a continuous probability

distribution. To illustrate, consider the simple spinning pointer in

Figure

spinner.

|

Spinner: a device for

generating a continuous random variable (in a zero-gravity, virtually

frictionless environment)

|

where all numbers in the

interval (0,4] are equally likely. The probability of the pointer stopping

precisely at the number

must be zero, because if not the total probability for

must be zero, because if not the total probability for

would be infinite, since the set

would be infinite, since the set

is non-countable. Thus, for a continuous random variable the probability at

each point is 0. This means we can no longer use the probability function to

describe a distribution. Instead there are two other functions commonly used

to describe continuous distributions.

is non-countable. Thus, for a continuous random variable the probability at

each point is 0. This means we can no longer use the probability function to

describe a distribution. Instead there are two other functions commonly used

to describe continuous distributions.

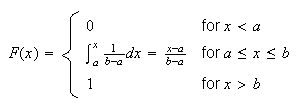

Cumulative Distribution Function:

For discrete random variables we defined the c.d.f.,

.

This function still works for continuous random variables. For the spinner,

the probability the pointer stops between 0 and 1 is 1/4 if all values

.

This function still works for continuous random variables. For the spinner,

the probability the pointer stops between 0 and 1 is 1/4 if all values

are equally ``likely"; between 0 and 2 the probability is 1/2, between 0 and 3

it is 3/4; and so on. In general,

are equally ``likely"; between 0 and 2 the probability is 1/2, between 0 and 3

it is 3/4; and so on. In general,

for

for

.

.

Also,

for

for

since there is no chance of the pointer stopping at a number

since there is no chance of the pointer stopping at a number

,

and

,

and

for

for

since the pointer is certain to stop at number below

since the pointer is certain to stop at number below

if

if

.

.

Most properties of a c.d.f. are the same for continuous variables as for

discrete variables. These are:

1.

and and

|

2.

is a non-decreasing function of

is a non-decreasing function of

|

3.

. . |

Note that, as indicated before, for a continuous distribution, we have

.

Also, since the probability is 0 at each point:

.

Also, since the probability is 0 at each point:

(For a discrete random variable, each of these 4 probabilities could be

different.). For the continuous distributions in this chapter, we do not

worry about whether intervals are open, closed, or half-open since the

probability of these intervals is the

same.

(For a discrete random variable, each of these 4 probabilities could be

different.). For the continuous distributions in this chapter, we do not

worry about whether intervals are open, closed, or half-open since the

probability of these intervals is the

same.

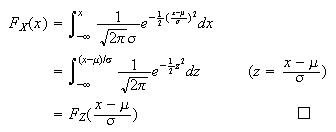

Probability Density Function (p.d.f.): While the c.d.f.

can be used to find probabilities, it does not give an intuitive picture of

which values of

are more likely, and which are less likely. To develop such a picture suppose

that we take a short interval of

are more likely, and which are less likely. To develop such a picture suppose

that we take a short interval of

-values,

-values,

![$[x,x+\Delta x]$](graphics/noteschap9__27.png) .

The probability

.

The probability

lies in the interval is

lies in the interval is

To compare the probabilities for two intervals, each of length

To compare the probabilities for two intervals, each of length

,

is easy. Now suppose we consider what happens as

,

is easy. Now suppose we consider what happens as

becomes small, and we divide the probability by

becomes small, and we divide the probability by

.

This leads to the following definition.

.

This leads to the following definition.

We will see that

represents the relative likelihood of different

represents the relative likelihood of different

-values.

To do this we first note some properties of a p.d.f. It is assumed that

-values.

To do this we first note some properties of a p.d.f. It is assumed that

is a continuous function of

is a continuous function of

at all points for which

at all points for which

.

.

Properties of a probability density function

-

This

follows from the definition of

.

.

-

(Since

is non-decreasing).

is non-decreasing).

-

This

is because

.

.

-

.

.

This is just property 1 with

.

.

To see that

represents the relative likelihood of different outcomes, we note that for

represents the relative likelihood of different outcomes, we note that for

small,

small,

Thus,

Thus,

but

but

is the approximate probability that

is the approximate probability that

is inside the interval

is inside the interval

![$[x,x+\Delta x]$](graphics/noteschap9__57.png) .

A plot of the function

.

A plot of the function

shows such values clearly and for this reason it is very common to plot the

p.d.f.'s of continuous random variables.

shows such values clearly and for this reason it is very common to plot the

p.d.f.'s of continuous random variables.

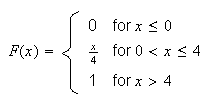

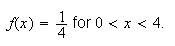

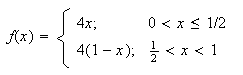

Example: Consider the spinner example, where

Thus, the p.d.f. is

Thus, the p.d.f. is

,

or

,

or

and outside this interval the p.d.f. is

and outside this interval the p.d.f. is

Figure

uniformpdf shows the probability density function

Figure

uniformpdf shows the probability density function

;

for obvious reasons this is called a "uniform" distribution.

;

for obvious reasons this is called a "uniform" distribution.

|

Uniform p.d.f.

|

Remark: Continuous probability distributions are, like

discrete distributions, mathematical models. Thus, the

distribution assumed for the spinner above is a model, though it seems likely

it would be a good model for many real spinners.

Remark: It may seem paradoxical that

for a continuous r.v. and yet we record the outcomes

for a continuous r.v. and yet we record the outcomes

in real "experiments" with continuous variables. The catch is that all

measurements have finite precision; they are in effect discrete. For example,

the height

in real "experiments" with continuous variables. The catch is that all

measurements have finite precision; they are in effect discrete. For example,

the height

inches is within the range of the height

inches is within the range of the height

of people in a population but we could never observe the outcome

of people in a population but we could never observe the outcome

if we selected a person at random and measured their height.

if we selected a person at random and measured their height.

To summarize, in measurements we are actually observing something like

where

where

may be very small, but not zero. The probability of this outcome is

not zero: it is (approximately)

may be very small, but not zero. The probability of this outcome is

not zero: it is (approximately)

.

.

We now consider a more complicated mathematical example of a continuous random

variable Then we'll consider real problems that involve continuous variables.

Remember that it is always a good idea to sketch or plot the p.d.f.

for a r.v.

for a r.v.

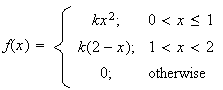

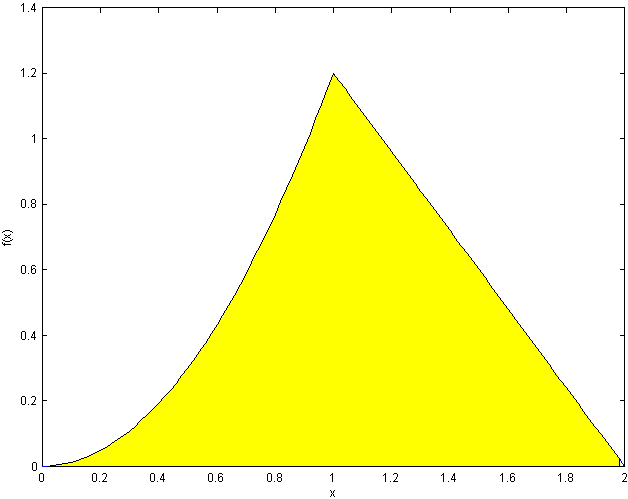

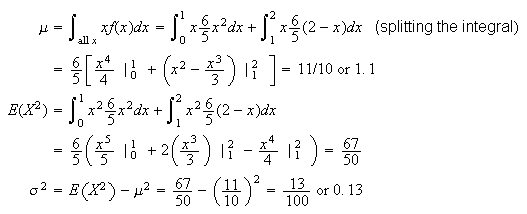

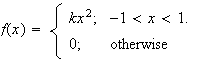

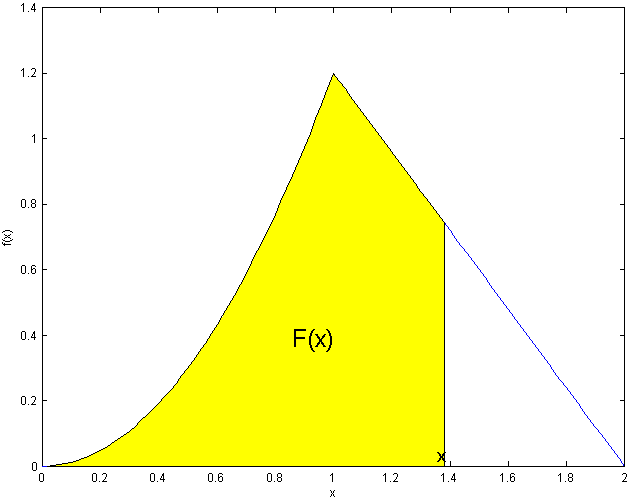

Example:

Let

be a p.d.f.

be a p.d.f.

Find

-

-

-

Solution:

-

Set

to solve for

to solve for

.

When finding the area of a region bounded by different functions we split the

integral into pieces.

.

When finding the area of a region bounded by different functions we split the

integral into pieces.

(We normally wouldn't even write down the parts with

)

)

-

Doing the easy pieces, which are often left out, first:

(see shaded area

below)

i.e.

As a rough check, since for a continuous distribution there is no probability

at any point,

should have the same value as we approach each boundary point from above and

from below.

should have the same value as we approach each boundary point from above and

from below.

e.g.

This quick check won't prove your answer is right, but will detect many

careless errors.

-

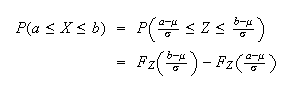

Defined Variables or Change of Variable:

When we know the

p.d.f. or c.d.f. for a continuous random variable

we sometimes want to find the p.d.f. or c.d.f. for some other random variable

we sometimes want to find the p.d.f. or c.d.f. for some other random variable

which is a function of

which is a function of

.

The procedure for doing this is summarized below. It is based on the fact that

the c.d.f.

.

The procedure for doing this is summarized below. It is based on the fact that

the c.d.f.

for

for

equals

equals

,

and this can be rewritten in terms of

,

and this can be rewritten in terms of

since

since

is a function of

is a function of

.

Thus:

.

Thus:

-

Write the c.d.f. of

as a function of

as a function of

.

.

-

Use

to find

to find

.

Then if you want the p.d.f.

.

Then if you want the p.d.f.

,

you can differentiate the expression for

,

you can differentiate the expression for

.

.

-

Find the range of values of

.

.

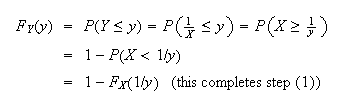

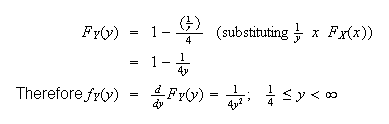

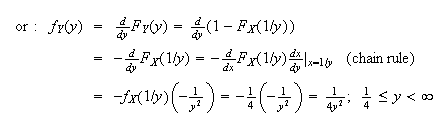

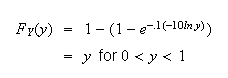

Example: In the earlier spinner example,

Let

Let

.

Find

.

Find

.

.

Solution:

For step (2), we can do either:

For step (2), we can do either:

(As

(As

goes from 0 to 4,

goes from 0 to 4,

goes between

goes between

and

and

.)

.)

Generally if

Generally if

is known it is easier to substitute first, then differentiate. If

is known it is easier to substitute first, then differentiate. If

is in the form of an integral that can't be solved, it is usually easier to

differentiate first, then substitute

is in the form of an integral that can't be solved, it is usually easier to

differentiate first, then substitute

.

.

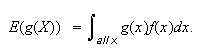

Extension of Expectation, Mean, and Variance to Continuous

Distributions

Definition

When

is continuous, we still define

is continuous, we still define

With this definition, all of the earlier properties of expectation and

variance still hold; for example with

(This definition can be justified by writing

as a limit of a Riemann sum and recognizing the Riemann sum as being in the

form of an expectation for discrete random

variables.)

as a limit of a Riemann sum and recognizing the Riemann sum as being in the

form of an expectation for discrete random

variables.)

Example: In the spinner example with

Example: Let

have p.d.f.

have p.d.f.

Then

Then

Problems:

-

Let

have p.d.f.

have p.d.f.

Find

Find

-

-

the c.d.f.,

-

-

the mean and variance of

.

.

-

let

.

Derive the p.d.f. of

.

Derive the p.d.f. of

.

.

-

A continuous distribution has c.d.f.

for

for

,

where

,

where

is a positive constant.

is a positive constant.

-

Evaluate

.

.

-

Find the p.d.f.,

.

.

-

What is the median of this distribution? (The median is the value of

such that half the time we get a value below it and half the time above it.)

such that half the time we get a value below it and half the time above it.)

Continuous Uniform Distribution

Just as we did for discrete r.v.'s, we now consider some special types of

continuous probability distributions. These distributions arise in certain

settings, described below. This section considers what we call uniform

distributions.

Physical Setup:

Suppose

takes values in some interval [a,b] (it doesn't actually matter whether

interval is open or closed) with all subintervals of a fixed length being

equally likely. Then

takes values in some interval [a,b] (it doesn't actually matter whether

interval is open or closed) with all subintervals of a fixed length being

equally likely. Then

has a continuous uniform distribution. We write

has a continuous uniform distribution. We write

.

.

Illustrations:

-

In the spinner example

![$X \sim U (0,4]$](graphics/noteschap9__155.png) .

.

-

Computers can generate a random number

which appears as though it is drawn from the distribution

which appears as though it is drawn from the distribution

.

This is the starting point for many computer simulations of random processes;

an example is given below.

.

This is the starting point for many computer simulations of random processes;

an example is given below.

The probability density function and the cumulative distribution

function:

Since all points are equally likely (more precisely, intervals contained in

![$[a,b]$](graphics/noteschap9__158.png) of a given length, say 0.01, all have the same probability), the probability

density function must be a constant

of a given length, say 0.01, all have the same probability), the probability

density function must be a constant

for some constant

for some constant

.

To make

.

To make

,

we require

,

we require

.

.

Mean and

Variance:

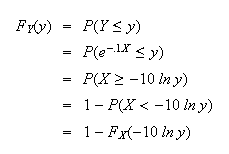

Example: Suppose

has the continuous p.d.f.

has the continuous p.d.f.

(This is called an exponential distribution and is discussed in the next

section. It is used in areas such as queueing theory and reliability.) We'll

show that the new random variable

(This is called an exponential distribution and is discussed in the next

section. It is used in areas such as queueing theory and reliability.) We'll

show that the new random variable

has a uniform distribution,

has a uniform distribution,

.

To see this, we follow the steps in Section

9.1:

.

To see this, we follow the steps in Section

9.1:

Since

we get

we get

(The range of

is (0,1) since

is (0,1) since

.)

Thus

.)

Thus

and so

and so

.

.

Many computer software systems have ``random number generator" functions that

will simulate observations

from a

from a

distribution. (These are more properly called pseudo-random number

generators because they are based on deterministic algorithms. In

addition they give observations

distribution. (These are more properly called pseudo-random number

generators because they are based on deterministic algorithms. In

addition they give observations

that have finite precision so they cannot be exactly like

continuous

that have finite precision so they cannot be exactly like

continuous

random variables. However, good generators give

random variables. However, good generators give

's

that appear indistinguishable in most ways from

's

that appear indistinguishable in most ways from

r.v.'s.) Given such a generator, we can also simulate r.v.'s

r.v.'s.) Given such a generator, we can also simulate r.v.'s

with the exponential distribution above by the following algorithm:

with the exponential distribution above by the following algorithm:

-

Generate

using the computer random number generator.

using the computer random number generator.

-

Compute

.

.

Then

has the desired distribution. This is a particular case of a method described

in Section 9.4 for generating random variables from a general distribution. In

has the desired distribution. This is a particular case of a method described

in Section 9.4 for generating random variables from a general distribution. In

software the command

software the command

produces a vector consisting of

produces a vector consisting of

independent

independent

values.

values.

Problem:

-

If

has c.d.f.

has c.d.f.

,

then

,

then

has a uniform distribution on [0,1]. (Show this.) Suppose you want to simulate

observations from a distribution with

has a uniform distribution on [0,1]. (Show this.) Suppose you want to simulate

observations from a distribution with

,

by using the random number generator on a computer to generate

,

by using the random number generator on a computer to generate

numbers. What value would

numbers. What value would

take when you generated the random number .27125?

take when you generated the random number .27125?

Exponential Distribution

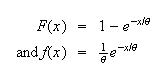

The continuous random variable

is said to have an exponential distribution if its p.d.f. is

of the form

is said to have an exponential distribution if its p.d.f. is

of the form

where

where

is a real parameter value. This distribution arises in various problems

involving the time until some event occurs. The following gives one such

setting.

is a real parameter value. This distribution arises in various problems

involving the time until some event occurs. The following gives one such

setting.

Physical Setup: In a Poisson process for events in time let

be the length of time we wait for the first event occurrence. We'll show that

be the length of time we wait for the first event occurrence. We'll show that

has an exponential distribution. (Recall that the number of occurrences

in a fixed time has a Poisson distribution. The difference between the Poisson

and exponential distributions lies in what is being

measured.)

has an exponential distribution. (Recall that the number of occurrences

in a fixed time has a Poisson distribution. The difference between the Poisson

and exponential distributions lies in what is being

measured.)

Illustrations:

-

The length of time

we wait with a Geiger counter until the emission of a radioactive particle is

recorded follows an exponential distribution.

we wait with a Geiger counter until the emission of a radioactive particle is

recorded follows an exponential distribution.

-

The length of time between phone calls to a fire station (assuming calls

follow a Poisson process) follows an exponential distribution.

Derivation of the probability density function and the c.d.f.

|

= |

(time to

(time to

occurrence

occurrence

) ) |

|

= |

(time to

(time to

occurrence

occurrence

)

) |

|

= |

(no occurrences in the interval

(no occurrences in the interval

) ) |

Check that you understand this last step. If the time to the first occurrence

,

there must be no occurrences in

,

there must be no occurrences in

,

and vice versa.

,

and vice versa.

We have now expressed

in terms of the number of occurrences in a Poisson process by time

in terms of the number of occurrences in a Poisson process by time

.

But the number of occurrences has a Poisson distribution with mean

.

But the number of occurrences has a Poisson distribution with mean

,

where

,

where

is the average rate of occurrence.

is the average rate of occurrence.

Since

Since

for

for

.

Thus

.

Thus which is the formula we gave above.

which is the formula we gave above.

Alternate Form: It is common to use the parameter

in the exponential distribution. (We'll see below that

in the exponential distribution. (We'll see below that

.)

This makes

.)

This makes

Exercise:

Suppose trees in a forest are distributed according to a Poisson process. Let

be the distance from an arbitrary starting point to the nearest tree. The

average number of trees per square metre is

be the distance from an arbitrary starting point to the nearest tree. The

average number of trees per square metre is

.

Derive

.

Derive

the same way we derived the exponential p.d.f. You're now using the Poisson

distribution in 2 dimensions (area) rather than 1 dimension

(time).

the same way we derived the exponential p.d.f. You're now using the Poisson

distribution in 2 dimensions (area) rather than 1 dimension

(time).

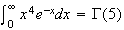

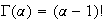

Mean and Variance:

Finding

and

and

directly involves integration by parts. An easier solution uses properties of

gamma functions, which extends the notion of factorials

beyond the integers to the positive real numbers.

directly involves integration by parts. An easier solution uses properties of

gamma functions, which extends the notion of factorials

beyond the integers to the positive real numbers.

Note that

is 1 more than the power of

is 1 more than the power of

in the integrand. e.g.

in the integrand. e.g.

.

There are 3 properties of gamma functions which we'll use.

.

There are 3 properties of gamma functions which we'll use.

-

for

for

Proof:

Using integration by parts,

and provided that

and provided that

Therefore

Therefore

-

if

if

is a positive integer.

is a positive integer.

Proof: It is easy to show that

Using property 1. repeatedly, we obtain

Using property 1. repeatedly, we obtain

etc.

etc.

Generally,.

for integer

for integer

-

(This

can be proved using double

integration.)

Returning to the exponential distribution:

Let

Let

.

Then

.

Then

and

and

Note: Read questions carefully. If you're given the average

rate of occurrence in a Poisson process, that is

.

If you're given the average time you wait for an occurrence,

that is

.

If you're given the average time you wait for an occurrence,

that is

.

.

To get

,

we first find

,

we first find

Example:

Suppose #7 buses arrive at a bus stop according to a Poisson process with an

average of 5 buses per hour. (i.e.

/hr.

So

/hr.

So

hr. or 12 min.) Find the probability (a) you have to wait longer than 15

minutes for a bus (b) you have to wait more than 15 minutes longer, having

already been waiting for 6 minutes.

hr. or 12 min.) Find the probability (a) you have to wait longer than 15

minutes for a bus (b) you have to wait more than 15 minutes longer, having

already been waiting for 6 minutes.

Solution:

-

=

-

If

is the total waiting time, the question asks for the probability

is the total waiting time, the question asks for the probability

Does this surprise you? The fact that you're already waited 6 minutes doesn't

seem to matter. This illustrates the ``memoryless property'' of the

exponential distribution:

Does this surprise you? The fact that you're already waited 6 minutes doesn't

seem to matter. This illustrates the ``memoryless property'' of the

exponential distribution:

Fortunately, buses don't follow a Poisson process so this example needn't

cause you to stop using the bus.

Fortunately, buses don't follow a Poisson process so this example needn't

cause you to stop using the bus.

Problems:

-

In a bank with on-line terminals, the time the system runs between disruptions

has an exponential distribution with mean

hours. One quarter of the time the system shuts down within 8 hours of the

previous disruption. Find

hours. One quarter of the time the system shuts down within 8 hours of the

previous disruption. Find

.

.

-

Flaws in painted sheets of metal occur over the surface according to the

conditions for a Poisson process, at an intensity of

per

per

.

Let

.

Let

be the distance from an arbitrary starting point to the second closest flaw.

(Assume sheets are of infinite size!)

be the distance from an arbitrary starting point to the second closest flaw.

(Assume sheets are of infinite size!)

-

Find the p.d.f.,

.

.

-

What is the average distance to the second closest flaw?

A Method for Computer Generation of Random Variables.

Most computer software has a built-in "pseudo-random number generator" that

will simulate observations

from a

from a

distribution, or at least a reasonable approximation to this uniform

distribution. If we wish a random variable with a non-uniform distribution,

the standard approach is to take a suitable function of

distribution, or at least a reasonable approximation to this uniform

distribution. If we wish a random variable with a non-uniform distribution,

the standard approach is to take a suitable function of

By far the simplest and most common method for generating non-uniform variates

is based on the inverse cumulative distribution function. For arbitrary c.d.f.

By far the simplest and most common method for generating non-uniform variates

is based on the inverse cumulative distribution function. For arbitrary c.d.f.

,

define

,

define

min

min .

This is a real inverse (i.e.

.

This is a real inverse (i.e.

)

in the case that the c.d.f. is continuous and strictly increasing, so for

example for a continuous distribution. However, in the more general case of a

possibly discontinuous non-decreasing c.d.f. (such as the c.d.f. of a discrete

distribution) the function continues to enjoy at least some of the properties

of an inverse.

)

in the case that the c.d.f. is continuous and strictly increasing, so for

example for a continuous distribution. However, in the more general case of a

possibly discontinuous non-decreasing c.d.f. (such as the c.d.f. of a discrete

distribution) the function continues to enjoy at least some of the properties

of an inverse.

is useful for generating a random variables having c.d.f.

is useful for generating a random variables having c.d.f.

from

from

a uniform random variable on the interval

a uniform random variable on the interval

![$[0,1].$](graphics/noteschap9__281.png)

Proof:

The proof is a consequence of the fact that

You can check this graphically be checking, for example, that if

You can check this graphically be checking, for example, that if

![$[U<F(x)]$](graphics/noteschap9__288.png) then

then

![$[F^{-1}(U)\leq x]$](graphics/noteschap9__289.png) (this confirms the left hand

"

(this confirms the left hand

" Taking probabilities on all sides of this, and using the fact that

Taking probabilities on all sides of this, and using the fact that

,

we discover that

,

we discover that

![$P[X\leq x]=F(x).$](graphics/noteschap9__292.png)

|

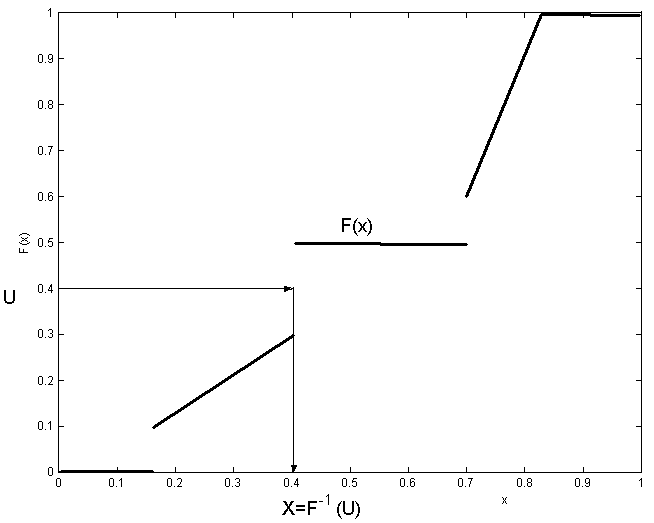

Inverting a c.d.f.

|

The relation

implies that

implies that

and for any point

and for any point

For example, for the rather unusual looking piecewise linear cumulative

distribution function in Figure inversetransform, we

find the solution

For example, for the rather unusual looking piecewise linear cumulative

distribution function in Figure inversetransform, we

find the solution

by drawing a horizontal line at

by drawing a horizontal line at

until it strikes the graph of the c.d.f. (or where the graph would have been

if we had joined the ends at the jumps) and then

until it strikes the graph of the c.d.f. (or where the graph would have been

if we had joined the ends at the jumps) and then

is the

is the

of this point. This is true in general,

of this point. This is true in general,

is the coordinate of the point where a horizontal line first strikes the graph

of the c.d.f. We provide one simple example of generating random variables by

this method, for the geometric distribution.

is the coordinate of the point where a horizontal line first strikes the graph

of the c.d.f. We provide one simple example of generating random variables by

this method, for the geometric distribution.

Example: A geometric random number generator

For the Geometric distribution, the cumulative distribution function is given

by

Then if

is a uniform random number in the interval

is a uniform random number in the interval

![$[0,1],$](graphics/noteschap9__305.png) we seek an integer

we seek an integer

such that

such that

(you should confirm that this is the value of

(you should confirm that this is the value of

at which the above horizontal line strikes the graph of the c.d.f) and solving

these inequalities gives

at which the above horizontal line strikes the graph of the c.d.f) and solving

these inequalities gives

so we compute the value of

so we compute the value of

and round down to the next lower integer.

and round down to the next lower integer.

Exercise: An exponential random number generator.

Show that the inverse transform method above results in the generator for the

exponential distribution

Normal Distribution

Physical Setup:

A random variable

defined on

defined on

has a normal distribution if it has probability density function of the form

has a normal distribution if it has probability density function of the form

where

where

and

and

are parameters. It turns out (and is shown below) that

are parameters. It turns out (and is shown below) that

and

Var

and

Var for this distribution; that is why its p.d.f. is written using the symbols

for this distribution; that is why its p.d.f. is written using the symbols

and

and

.

We write

.

We write

to denote that

to denote that

has a normal distribution with mean

has a normal distribution with mean

and variance

and variance

(standard deviation

(standard deviation

).

).

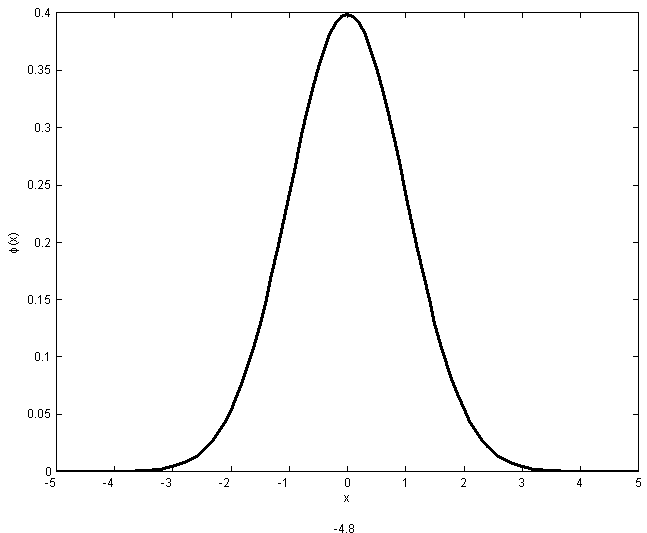

The normal distribution is the most widely used distribution in probability

and statistics. Physical processes leading to the normal distribution exist

but are a little complicated to describe. (For example, it arises in physics

via statistical mechanics and maximum entropy arguments.) It is used for many

processes where

represents a physical dimension of some kind, but also in many other settings.

We'll see other applications of it below. The shape of the p.d.f.

represents a physical dimension of some kind, but also in many other settings.

We'll see other applications of it below. The shape of the p.d.f.

above is what is often termed a ``bell shape'' or ``bell curve'', symmetric

about

above is what is often termed a ``bell shape'' or ``bell curve'', symmetric

about

as shown in Figure normpdf.(you should be able to

verify the shape without graphing the function)

as shown in Figure normpdf.(you should be able to

verify the shape without graphing the function)

|

The standard normal

probability density function

|

Illustrations:

-

Heights or weights of males (or of females) in large populations tend to

follow normal distributions.

-

The logarithms of stock prices are often assumed to be normally distributed.

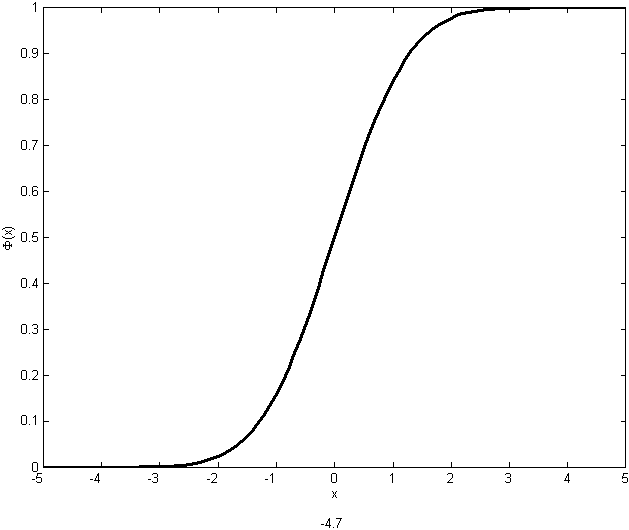

The cumulative distribution function: The c.d.f. of the

normal distribution

is

is

as shown in Figure normcdf. This integral cannot be

given a simple mathematical expression so numerical methods are used to

compute its value for given values of

as shown in Figure normcdf. This integral cannot be

given a simple mathematical expression so numerical methods are used to

compute its value for given values of

and

and

.

This function is included in many software packages and some calculators.

.

This function is included in many software packages and some calculators.

|

The standard normal c.d.f.

|

In the statistical packages

and

and

-Plus

we get

-Plus

we get

above using the function

above using the function

.

.

Before computers, people produced tables of probabilities

using mechanical calculators. Fortunately it is necessary to do this only for

a single normal distribution: the one with

using mechanical calculators. Fortunately it is necessary to do this only for

a single normal distribution: the one with

and

and

.

This is called the ``standard" normal distribution and

denoted

.

This is called the ``standard" normal distribution and

denoted

.

.

Its easy to see that if

then the "new" r.v.

then the "new" r.v.

is distributed as

is distributed as

.

(Just use the change of variables methods in Section 9.1.) We'll use this to

compute

.

(Just use the change of variables methods in Section 9.1.) We'll use this to

compute

and probabilities for

and probabilities for

below, but first we show that

below, but first we show that

integrates to 1 and that

integrates to 1 and that

and

Var

and

Var .

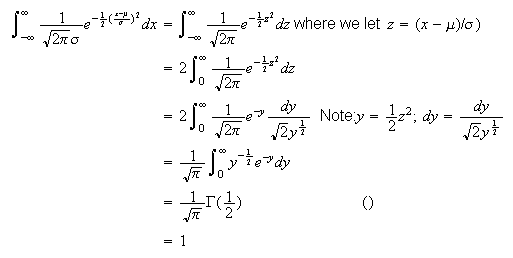

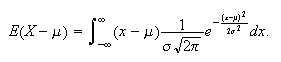

For the first result, note

that

.

For the first result, note

that

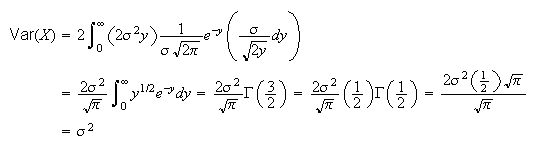

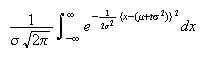

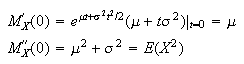

Mean, Variance, Moment generating function: Recall that an

odd function,

,

has the property that

,

has the property that

.

If

.

If

is an odd function then

is an odd function then

,

provided the integral exists.

,

provided the integral exists.

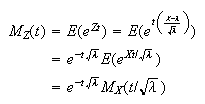

Consider

Let

.

Then

.

Then

where

is an odd function so that

is an odd function so that

.

But since

.

But since

,

this implies

,

this implies

and so

and so

is the mean. To obtain the variance,

is the mean. To obtain the variance,

We can obtain a gamma function by letting

We can obtain a gamma function by letting

.

.

Then

Then

and so

and so

is the variance. We now find the moment generating function of the

is the variance. We now find the moment generating function of the

distribution. If

distribution. If

has the

has the

distribution, then

distribution, then

where the last step follows since

where the last step follows since

is just the integral of a

is just the integral of a

probability density function and is therefore equal to one. This confirms the

values we already obtained for the mean and the variance of the normal

distribution

probability density function and is therefore equal to one. This confirms the

values we already obtained for the mean and the variance of the normal

distribution

from which we obtain

from which we obtain

Finding Normal Probabilities Via

Tables As noted above,

Tables As noted above,

does not have an explicit closed form so numerical computation is needed. The

following result shows that if we can compute the c.d.f. for the standard

normal distribution

does not have an explicit closed form so numerical computation is needed. The

following result shows that if we can compute the c.d.f. for the standard

normal distribution

,

then we can compute it for any other normal distribution

,

then we can compute it for any other normal distribution

as well.

as well.

Proof: The fact that

has p.d.f.

has p.d.f.

follows immediately by change of variables. Alternatively, we can just note

that

follows immediately by change of variables. Alternatively, we can just note

that

A table of probabilities

is given on the last page of these notes. A space-saving feature is that only

the values for

is given on the last page of these notes. A space-saving feature is that only

the values for

are shown; for negative values we use the fact that

are shown; for negative values we use the fact that

p.d.f. is symmetric about 0.

p.d.f. is symmetric about 0.

The following examples illustrate how to get probabilities for

using the tables.

using the tables.

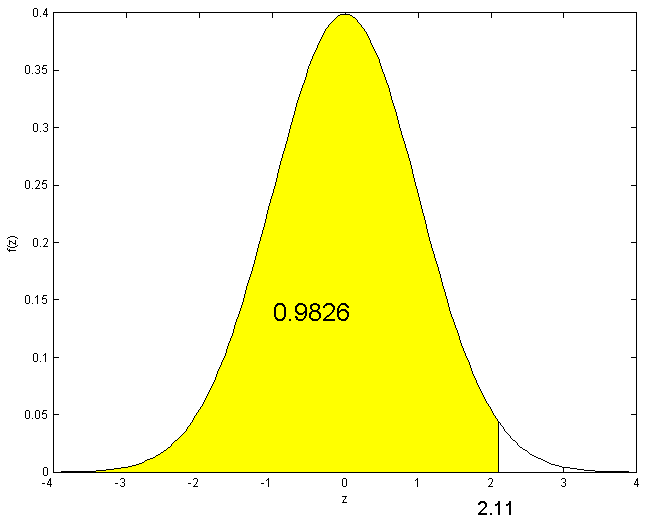

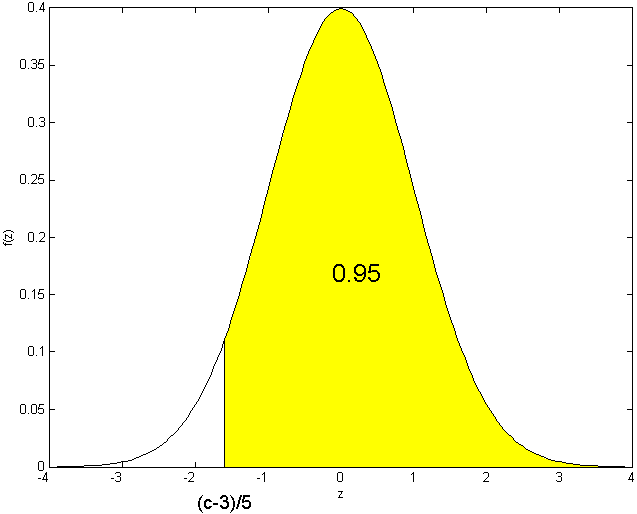

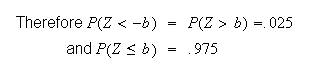

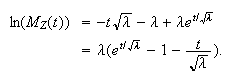

Examples: Find the following probabilities, where

.

.

-

-

-

-

-

Solution:

-

Look up 2.11 in the table by going down the left column to 2.1 then across to

the heading .01. We find the number .9826. Then

.

See Figure exercisenormal1.

.

See Figure exercisenormal1.

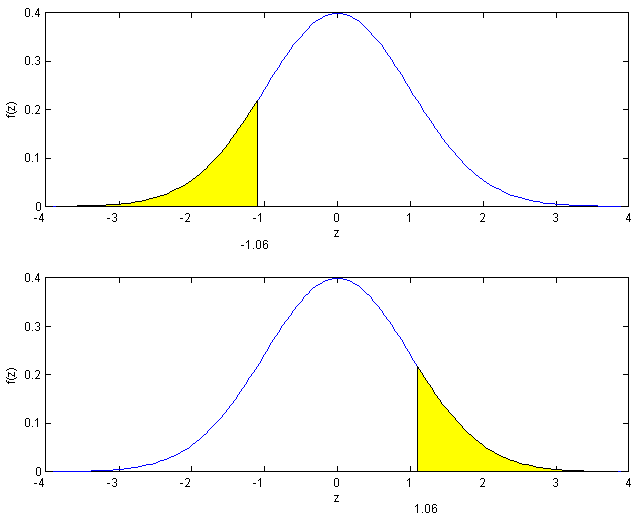

-

-

-

Now we have to use symmetry:

See Figure exercisenormal2.

See Figure exercisenormal2.

-

In addition to using the tables to find the probabilities for given numbers,

we sometimes are given the probabilities and asked to find the number. With

or

or

-Plus

software , the function qnorm

-Plus

software , the function qnorm

gives the 100

gives the 100

-th

percentile (where

-th

percentile (where

.

We can also use tables to find desired values.

.

We can also use tables to find desired values.

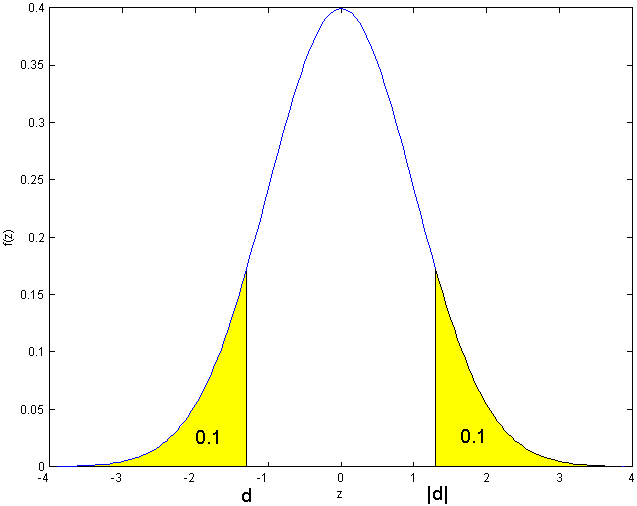

Examples:

-

Find a number

such that

such that

-

Find a number

such that

such that

-

Find a number

such that

such that

Solutions:

-

We can look in the body of the table to get an entry close to .8500. This

occurs for

between 1.03 and 1.04;

between 1.03 and 1.04;

gives the closest value to .85. For greater accuracy, the table at the bottom

of the last page is designed for finding numbers, given the probability.

Looking beside the entry .85 we find

gives the closest value to .85. For greater accuracy, the table at the bottom

of the last page is designed for finding numbers, given the probability.

Looking beside the entry .85 we find

.

.

-

Since

we have

we have

.

There is no entry for which

.

There is no entry for which

so we again have to use symmetry, since

so we again have to use symmetry, since

will be negative.

will be negative.

The key to this solution lies in recognizing that

will be negative. If you can picture the situation it will probably be easier

to handle the question than if you rely on algebraic

manipulations.

will be negative. If you can picture the situation it will probably be easier

to handle the question than if you rely on algebraic

manipulations.

Exercise: Will

be positive or negative if

be positive or negative if

?

What if

?

What if

?

?

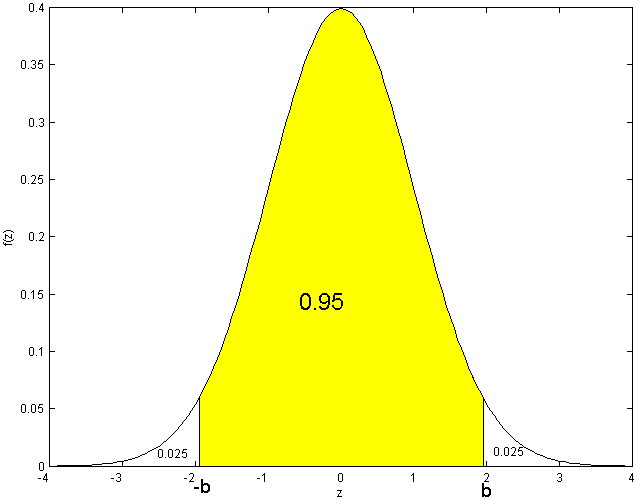

-

If

we again use

symmetry.

we again use

symmetry.

The probability outside the interval

must be .05, and this is evenly split between the area above

must be .05, and this is evenly split between the area above

and the area below

and the area below

.

.

Looking in the table,

.

.

To find

probabilities in general, we use the theorem given earlier, which implies that

if

probabilities in general, we use the theorem given earlier, which implies that

if

then

then

where

where

.

.

Example: Let

.

.

-

Find

-

Find a number

such that

such that

.

.

Solution:

-

-

Gaussian Distribution: The normal distribution is also known

as the Gaussian Note_1

distribution. The notation

Gaussian Distribution: The normal distribution is also known

as the Gaussian Note_1

distribution. The notation

means that

means that

has Gaussian (normal) distribution with mean

has Gaussian (normal) distribution with mean

and standard deviation

and standard deviation

.

So, for example, if

.

So, for example, if

then we could also write

then we could also write

.

.

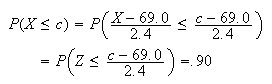

Example: The heights of adult males in Canada are close to

normally distributed, with a mean of 69.0 inches and a standard deviation of

2.4 inches. Find the 10th and 90th percentiles of the height distribution.

(Recall that the a-th percentile is such that a% of the population has height

less that this value.)

Solution: We are being told that if

is the height of a randomly selected Canadian adult male, then

is the height of a randomly selected Canadian adult male, then

,

or equivalently

,

or equivalently

.

To find the 90th percentile

.

To find the 90th percentile

,

we

use

,

we

use From the table we see

From the table we see

so we need

so we need

which gives

which gives

inches. Similarly, to find

inches. Similarly, to find

such that

such that

we find that

we find that

,

so we need

,

so we need

or

or

inches, as the 10th percentile.

inches, as the 10th percentile.

Linear Combinations of Independent Normal Random Variables

Linear combinations of normal r.v.'s are important in many applications. Since

we have not covered continuous multivariate distributions, we can only quote

the second and third of the following results without proof. The first result

follows easily from the change of variables method.

-

Let

and

and

,

where

,

where

and

and

are constant real numbers. Then

are constant real numbers. Then

-

Let

and

and

be independent, and let

be independent, and let

and

and

be constants.

be constants.

Then

.

.

In

general if

are independent and

are independent and

are constants,

are constants,

then

.

.

-

Let

be independent

be independent

random variables.

random variables.

Then

and

and

.

.

Actually, the only new result here is that the distributions are normal. The

means and variances of linear combinations of r.v.'s were previously obtained

in section 8.3.

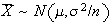

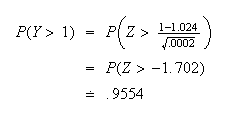

Example: Let

and

and

be independent. Find

be independent. Find

.

.

Solution: Whenever we have variables on both sides of the

inequality we should collect them on one side, leaving us with a linear

combination.

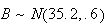

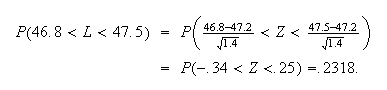

Example: Three cylindrical parts are joined end to end to

make up a shaft in a machine; 2 type A parts and 1 type B. The lengths of the

parts vary a little, and have the distributions:

and

and

.

The overall length of the assembled shaft must lie between 46.8 and 47.5 or

else the shaft has to be scrapped. Assume the lengths of different parts are

independent. What percent of assembled shafts have to be scrapped?

.

The overall length of the assembled shaft must lie between 46.8 and 47.5 or

else the shaft has to be scrapped. Assume the lengths of different parts are

independent. What percent of assembled shafts have to be scrapped?

Exercise: Why would it be wrong to represent the length of

the shaft as 2A + B? How would this length differ from the solution given

below?

Solution: Let

,

the length of the shaft, be

,

the length of the shaft, be

.

.

Then

and so

and so

i.e. 23.18% are acceptable and 76.82% must be scrapped. Obviously we have to

find a way to reduce the variability in the lengths of the parts. This is a

common problem in manufacturing.

Exercise: How could we reduce the percent of shafts being

scrapped? (What if we reduced the variance of

and

and

parts each by 50%?)

parts each by 50%?)

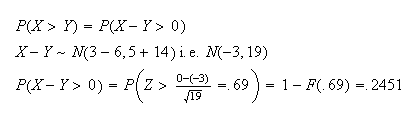

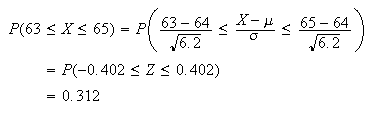

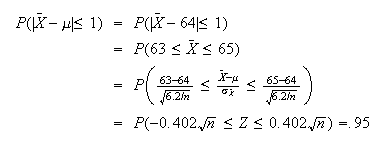

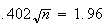

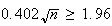

Example:

The heights of adult females in a large population is well represented by a

normal distribution with mean 64 in. and variance 6.2

in .

.

-

Find the proportion of females whose height is between 63 and 65 inches.

-

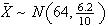

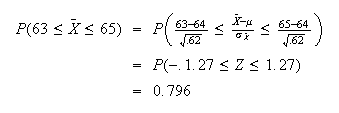

Suppose 10 women are randomly selected, and let

be their average height ( i.e.

be their average height ( i.e.

,

where

,

where

are the heights of the 10 women). Find

are the heights of the 10 women). Find

.

.

-

How large must

be so that a random sample of

be so that a random sample of

women gives an average height

women gives an average height

so that

so that

?

?

Solution:

-

so for the height

so for the height

of a random

woman,

of a random

woman,

-

so

so

-

If

then

then

iff

.

(This is because

.

(This is because

.

So

.

So

iff

iff

which is true if

which is true if

,

or

,

or

.

Thus we require

.

Thus we require

since

since

is an integer.

is an integer.

Remark: This shows that if we were to select a random sample

of

persons, then their average height

persons, then their average height

would be with 1 inch of the average height

would be with 1 inch of the average height

of the whole population of women. So if we did not know

of the whole population of women. So if we did not know

then we could estimate it to within

then we could estimate it to within

inch (with probability .95) by taking this small a

sample.

inch (with probability .95) by taking this small a

sample.

Exercise: Find how large

would have to be to make

would have to be to make

.

.

These ideas form the

basis of statistical sampling and estimation of unknown parameter values in

populations and processes. If

and we know roughly what

and we know roughly what

is, but don't know

is, but don't know

,

then we can use the fact that

,

then we can use the fact that

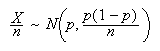

to find the probability that the mean

to find the probability that the mean

from a sample of size

from a sample of size

will be within a given distance of

will be within a given distance of

.

.

Problems:

-

Let

and

and

be independent. Find the probability

be independent. Find the probability

-

-

-

where

where

is the sample mean of 25 independent observations on

is the sample mean of 25 independent observations on

.

.

-

Let

have a normal distribution. What percent of the time does

have a normal distribution. What percent of the time does

lie within one standard deviation of the mean? Two standard deviations? Three

standard deviations?

lie within one standard deviation of the mean? Two standard deviations? Three

standard deviations?

-

Let

.

An independent variable

.

An independent variable

is also normally distributed with mean 7 and standard deviation 3. Find:

is also normally distributed with mean 7 and standard deviation 3. Find:

-

The probability

differs from

differs from

by more than 4.

by more than 4.

-

The minimum number,

,

of independent observations needed on

,

of independent observations needed on

so

that

so

that

is the sample mean)

is the sample mean)

Use of the Normal Distribution in Approximations

The normal distribution can, under certain conditions, be used to approximate

probabilities for linear combinations of variables having a non-normal

distribution. This remarkable property follows from an amazing result called

the central limit theorem. There are actually several versions of the central

limit theorem. The version given below is one of the

simplest.

Central Limit Theorem (CLT):

The major reason that the normal distribution is so commonly used is that it

tends to approximate the distribution of sums of random variables. For

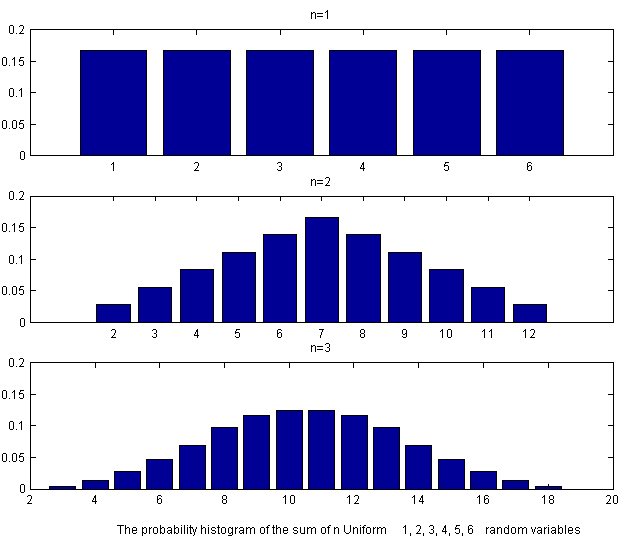

example, if we throw

fair dice and

fair dice and

is the sum of the outcomes, what is the distribution of

is the sum of the outcomes, what is the distribution of

The tables below provide the number of ways in which a given value can be

obtained. The corresponding probability is obtained by dividing by

The tables below provide the number of ways in which a given value can be

obtained. The corresponding probability is obtained by dividing by

For example on the throw of

For example on the throw of

dice the probable outcomes are 1,2,...,6 with probabilities all

dice the probable outcomes are 1,2,...,6 with probabilities all

as indicated in the first panel of the histogram in Figure

clt.

as indicated in the first panel of the histogram in Figure

clt.

The probability histogram of

the sum of

discrete uniform {1,2,3,4,5,6}Random variables

discrete uniform {1,2,3,4,5,6}Random variables

|

If we sum the values on two fair dice, the possible outcomes are the values

2,3,...,12 as shown in the following table and the probabilities are the

values below:

| Values |

2 |

3 |

4 |

5 |

6 |

7 |

8 |

9 |

10 |

11 |

12 |

Probabilities |

1 |

2 |

3 |

4 |

5 |

6 |

5 |

4 |

3 |

2 |

1 |

The probability histogram of these values is shown in the second panel.

Finally for the sum of the values on three independent dice, the values range

from 3 to 18 and have probabilities which, when multiplied by

result in the values

result in the values

to which we can fit three separate quadratic functions one in

the middle region and one in each of the two tails. The histogram of these

values shown in the third panel of Figure clt. and

already resembles a normal probability density function.In general, these

distributions show a simple pattern. For

,

the probability function is a constant (polynomial degree 0). For

,

the probability function is a constant (polynomial degree 0). For

two linear functions spliced together. For

two linear functions spliced together. For

,

the histogram can be constructed from three quadratic pieces (polynomials of

degree

,

the histogram can be constructed from three quadratic pieces (polynomials of

degree

These probability histograms rapidly approach the shape of the normal

probability density function, as is the case with the sum or the average of

independent random variables from most distributions. You can simulate the

throws of any number of dice and illustrate the behaviour of the sums on at

the url

http://www.math.csusb.edu/faculty/stanton/probstat/clt.html.

These probability histograms rapidly approach the shape of the normal

probability density function, as is the case with the sum or the average of

independent random variables from most distributions. You can simulate the

throws of any number of dice and illustrate the behaviour of the sums on at

the url

http://www.math.csusb.edu/faculty/stanton/probstat/clt.html.

Let

be independent random variables all having the same distribution, with mean

be independent random variables all having the same distribution, with mean

and variance

and variance

.

Then as

.

Then as

,

,

and

and

This is actually a rough statement of the result since, as

This is actually a rough statement of the result since, as

,

both the

,

both the

and

and

distributions fail to exist. (The former because both

distributions fail to exist. (The former because both

and

and

,

the latter because

,

the latter because

.)

A precise version of the results is:

.)

A precise version of the results is:

Although this is a theorem about limits, we will use it when

is large, but finite, to approximate the distribution of

is large, but finite, to approximate the distribution of

or

or

by a normal distribution, so the rough version of the theorem in

(cltsum) and (cltmean) is

adequate for our purposes.

by a normal distribution, so the rough version of the theorem in

(cltsum) and (cltmean) is

adequate for our purposes.

Notes:

-

This theorem works for essentially all distributions which

could have. The only exception occurs when

could have. The only exception occurs when

has a distribution whose mean or variance don't exist. There are such

distributions, but they are rare.

has a distribution whose mean or variance don't exist. There are such

distributions, but they are rare.

-

We will use the Central Limit Theorem to approximate the distribution of sums

or averages

or averages

.

The accuracy of the approximation depends on

.

The accuracy of the approximation depends on

(bigger is better) and also on the actual distribution the

(bigger is better) and also on the actual distribution the

's

come from. The approximation works better for small

's

come from. The approximation works better for small

when

when

's

p.d.f. is close to symmetric.

's

p.d.f. is close to symmetric.

-

If you look at the section on linear combinations of independent normal random

variables you will find two results which are very similar to the central

limit theorem. These are:

For

independent and

independent and

,

,

,

and

,

and

.

.

Thus, if the

's

themselves have a normal distribution, then

's

themselves have a normal distribution, then

and

and

have exactly normal distributions for all values of

have exactly normal distributions for all values of

.

If the

.

If the

's

do not have a normal distribution themselves, then

's

do not have a normal distribution themselves, then

and

and

have approximately normal distributions when

have approximately normal distributions when

is large. From this distinction you should be able to guess that if the

is large. From this distinction you should be able to guess that if the

's

distribution is somewhat normal shaped the approximation will be good for

smaller values of

's

distribution is somewhat normal shaped the approximation will be good for

smaller values of

than if the

than if the

's

distribution is very non-normal in shape. (This is related to the second

remark in (2)).

's

distribution is very non-normal in shape. (This is related to the second

remark in (2)).

Example: Hamburger patties are packed 8 to a box, and each

box is supposed to have 1 Kg of meat in it. The weights of the patties vary a

little because they are mass produced, and the weight

of a single patty is actually a random variable with mean

of a single patty is actually a random variable with mean

kg and standard deviation

kg and standard deviation

kg. Find the probability a box has at least 1 kg of meat, assuming that the

weights of the 8 patties in any given box are

independent.

kg. Find the probability a box has at least 1 kg of meat, assuming that the

weights of the 8 patties in any given box are

independent.

Solution: Let

be the weights of the 8 patties in a box, and

be the weights of the 8 patties in a box, and

be their total weight. By the Central Limit Theorem,

be their total weight. By the Central Limit Theorem,

is approximately

is approximately

;

we'll assume this approximation is reasonable even though

;

we'll assume this approximation is reasonable even though

is small. (This is likely ok because

is small. (This is likely ok because

's

distribution is likely fairly close to normal itself.) Thus

's

distribution is likely fairly close to normal itself.) Thus

and

and

(We see that only about 95% of the boxes actually have 1 kg or more of

hamburger. What would you recommend be done to increase this probability to

95%?)

(We see that only about 95% of the boxes actually have 1 kg or more of

hamburger. What would you recommend be done to increase this probability to

95%?)

Example: Suppose fires reported to a fire station satisfy

the conditions for a Poisson process, with a mean of 1 fire every 4 hours.

Find the probability the

fire of the year is reported on the

fire of the year is reported on the

day of the year.

day of the year.

Solution: Let

be the time between the

be the time between the

and

and

fires

(

fires

( is the time to the

is the time to the

fire). Then

fire). Then

has an exponential distribution with

has an exponential distribution with

hrs, or

hrs, or

day. Since

day. Since

is the time until the 500th fire, we want to find

is the time until the 500th fire, we want to find

.

While the exponential distribution is not close to normal shaped, we are

summing a large number of independent exponential variables. Hence, by the

central limit theorem,

.

While the exponential distribution is not close to normal shaped, we are

summing a large number of independent exponential variables. Hence, by the

central limit theorem,

has approximately a

has approximately a

distribution, where

distribution, where

and

and

.

.

For exponential distributions,

and

and

so

so

Example: This example is frivolous but shows how the normal

distribution can approximate even sums of discrete r.v.'s. In an orchard,

suppose the number

of worms in an apple has probability function:

of worms in an apple has probability function:

|

0 |

1 |

2 |

3 |

|

.4 |

.3 |

.2 |

.1 |

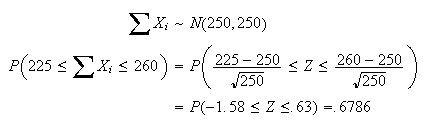

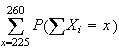

Find the probability a basket with 250 apples in it has between 225 and 260

(inclusive) worms in it.

Solution:

By the central limit theorem,

By the central limit theorem,

has approximately a

has approximately a

distribution, where

distribution, where

is the number of worms in the

is the number of worms in the

apple.

apple.

i.e.

While this approximation is adequate, we can improve its accuracy, as follows.

When

has a discrete distribution, as it does here,

has a discrete distribution, as it does here,

will always remain discrete no matter how large

will always remain discrete no matter how large

gets. So the distribution of

gets. So the distribution of

,

while normal shaped, will never be precisely normal. Consider a probability

histogram of the distribution of

,

while normal shaped, will never be precisely normal. Consider a probability

histogram of the distribution of

,

as shown in Figure p167. (Only part of the histogram

is shown.)

,

as shown in Figure p167. (Only part of the histogram

is shown.)

The area of each bar of this histogram is the probability at the

value in the centre of the interval. The smooth curve is the p.d.f. for the

approximating normal distribution. Then

value in the centre of the interval. The smooth curve is the p.d.f. for the

approximating normal distribution. Then

is the total area of all bars of the histogram for

is the total area of all bars of the histogram for

from 225 to 260. These bars actually span continuous

from 225 to 260. These bars actually span continuous

values from 224.5 to 260.5. We could then get a more accurate approximation by

finding the area under the normal curve from 224.5 to 260.5.

values from 224.5 to 260.5. We could then get a more accurate approximation by

finding the area under the normal curve from 224.5 to 260.5.

i.e.

Unless making this adjustment greatly complicates the solution, it is

preferable to make this "continuity

correction".

Unless making this adjustment greatly complicates the solution, it is

preferable to make this "continuity

correction".

Notes:

-

A continuity correction should not be applied when approximating a

continuous distribution by the normal distribution. Since it involves going

halfway to the next possible value of

,

there would be no adjustment to make if

,

there would be no adjustment to make if

takes real values.

takes real values.

-

Rather than trying to guess or remember when to add .5 and when to subtract

.5, it is often helpful to sketch a histogram and shade the bars we wish to

include. It should then be obvious which value to

use.

Example: Normal approximation to the Poisson Distribution

Let

be a random variable with a

Poisson

be a random variable with a

Poisson distribution and suppose

distribution and suppose

is large. For the moment suppose that

is large. For the moment suppose that

is an integer and recall that if we add

is an integer and recall that if we add

independent Poisson random variables, each with parameter

independent Poisson random variables, each with parameter

then the sum has the Poisson distribution with parameter

then the sum has the Poisson distribution with parameter

In general, a Poisson random variable with large expected value can be written

as the sum of a large number of independent random variables, and so the

central limit theorem implies that it must be close to normally distributed.

We can prove this using moment generating functions. In Section 7.5 we found

the moment generating function of a Poisson random variable

In general, a Poisson random variable with large expected value can be written

as the sum of a large number of independent random variables, and so the

central limit theorem implies that it must be close to normally distributed.

We can prove this using moment generating functions. In Section 7.5 we found

the moment generating function of a Poisson random variable

Then the standardized random variable is

Then the standardized random variable is

and this has moment generating function

and this has moment generating function

This is easier to work with if we take

logarithms,

This is easier to work with if we take

logarithms, Now as

Now as

and

and

so

so

Therefore the moment generating function of the standardized Poisson random

variable

Therefore the moment generating function of the standardized Poisson random

variable

approaches

approaches

the moment generating function of the standard normal and this implies that

the Poisson distribution approaches the normal as

the moment generating function of the standard normal and this implies that

the Poisson distribution approaches the normal as

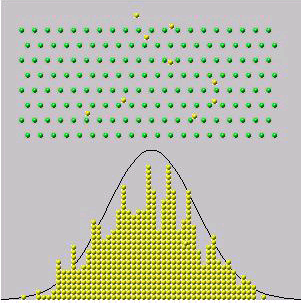

Normal approximation to the Binomial Distribution

It is well-known that the binomial distribution, at least for large values of

resembles a bell-shaped or normal curve. The most common demonstration of this

is with a mechanical device common in science museums called a "Galton board"

or "Quincunx" Note_2 which drop

balls through a mesh of equally spaced pins (see Figure

balldrop and the applet at

resembles a bell-shaped or normal curve. The most common demonstration of this

is with a mechanical device common in science museums called a "Galton board"

or "Quincunx" Note_2 which drop

balls through a mesh of equally spaced pins (see Figure

balldrop and the applet at

http://javaboutique.internet.com/BallDrop/). Notice

that if balls either go to the right or left at each of the 8 levels of pins,

independently of the movement of the other balls, then

number

of moves to right has a

number

of moves to right has a

distribution. If the balls are dropped from location

distribution. If the balls are dropped from location

(on the

(on the

axis)

then the ball eventually rests at location

axis)

then the ball eventually rests at location

which is approximately normally distributed since

which is approximately normally distributed since

is approximately normal.

is approximately normal.

|

A "Galton Board" or

"Quincunx"

|

The following result is easily proved using the Central Limit

Theorem.![$\bigskip$]()

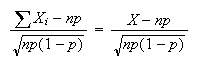

Proof: We use indicator variables

where

where

if the

if the

th

trial in the binomial process is an

"

th

trial in the binomial process is an

" " outcome

and 0 if it is an

"

" outcome

and 0 if it is an

" " outcome.

Then

" outcome.

Then

and we can use the CLT. Since

and we can use the CLT. Since

we have that as

we have that as

is

is

,

as stated. \framebox[0.10in]{}

,

as stated. \framebox[0.10in]{}

An alternative proof uses moment generating functions and is essentially a

proof of this particular case of the Central Limit Theorem. Recall that the

moment generating function of the binomial random variable

is

is

As we did with the standardized Poisson random variable, we can show with some

algebraic effort that the moment generating function of

As we did with the standardized Poisson random variable, we can show with some

algebraic effort that the moment generating function of

proving that the standardized binomial random variable

proving that the standardized binomial random variable

approaches the standard normal

distribution.

approaches the standard normal

distribution.![$\bigskip$]()

Remark: We can write the normal approximation either as

or as

or as

.

.![$\bigskip$]()

Remark: The continuity correction method can be used here.

The following numerical example illustrates the procedure.

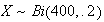

Example: If (i)

,

use the theorem to find the approximate probability

,

use the theorem to find the approximate probability

and (ii) if

and (ii) if

find the approximate probability

find the approximate probability

.

Compare the answer with the exact value in each

case.

.

Compare the answer with the exact value in each

case.![$\bigskip$]()

Solution (i) By the theorem above,

approximately. Without the continuity correction,

approximately. Without the continuity correction,

where

where

.

Using the continuity correction method, we get

.

Using the continuity correction method, we get

The exact probability is

The exact probability is

,

which (using the

,

which (using the

function

function

)

is .963. As expected the continuity correction method gives a more accurate

approximation.

)

is .963. As expected the continuity correction method gives a more accurate

approximation.

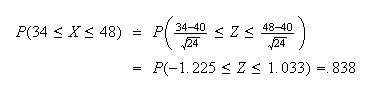

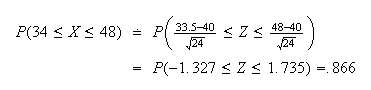

(ii)

approximately so without the continuity correction

approximately so without the continuity correction

With the continuity correction

With the continuity correction

The exact value,

The exact value,

,

equals .866 (to 3 decimals). The error of the normal approximation decreases

as

,

equals .866 (to 3 decimals). The error of the normal approximation decreases

as

increases, but it is a good idea to use the CC when it is

convenient.

increases, but it is a good idea to use the CC when it is

convenient.

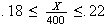

Example: Let

be the proportion of Canadians who think Canada should adopt the US dollar.

be the proportion of Canadians who think Canada should adopt the US dollar.

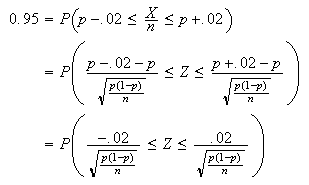

-

Suppose 400 Canadians are randomly chosen and asked their opinion. Let

be the number who say yes. Find the probability that the proportion,

be the number who say yes. Find the probability that the proportion,

,

of people who say yes is within .02 of

,

of people who say yes is within .02 of

,

if

,

if

is .20.

is .20.

-

Find the number,

,

who must be surveyed so there is a 95% chance that

,

who must be surveyed so there is a 95% chance that

lies within .02 of

lies within .02 of

.

Again suppose

.

Again suppose

is .20.

is .20.

-

Repeat (b) when the value of

is unknown.

is unknown.

Solution:

-

.

Using the normal approximation we take

.

Using the normal approximation we take

If

lies within

lies within

,

then

,

then

,

so

,

so

.

Thus, we find

.

Thus, we find

-

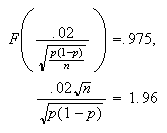

Since

is unknown, it is difficult to apply a continuity correction, so we omit it in

this part. By the normal approximation,

is unknown, it is difficult to apply a continuity correction, so we omit it in

this part. By the normal approximation,

Therefore,

Therefore,

is the condition we need to satisfy. This

gives

is the condition we need to satisfy. This

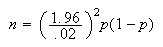

gives Therefore,

Therefore,

and so

and so

giving

giving

In other words, we need to survey 1537 people to be at least 95% sure that

In other words, we need to survey 1537 people to be at least 95% sure that

lies within .02 either side of

lies within .02 either side of

.

.

-

Now using the normal approximation to the binomial, approximately

and

so

and

so

We wish to find

We wish to find

such that

such that

As is part

(b),

As is part

(b), Solving for

Solving for

Unfortunately this does not give us an explicit expression for

Unfortunately this does not give us an explicit expression for

because we don't know

because we don't know

.

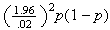

The way out of this dilemma is to find the maximum value

.

The way out of this dilemma is to find the maximum value

could take. If we choose

could take. If we choose

this large, then we can be sure of having the required precision in our

estimate,

this large, then we can be sure of having the required precision in our

estimate,

,

for any

,

for any

.

It's easy to see that

.

It's easy to see that

is a maximum when

is a maximum when

.

Therefore we take

.

Therefore we take

i.e., if we survey 2401 people we can be 95% sure that

i.e., if we survey 2401 people we can be 95% sure that

lies within .02 of

lies within .02 of

,

regardless of the value of

,

regardless of the value of

.

.

Remark: This method is used when poll results are reported

in the media: you often see or hear that "this poll is accurate to with 3

percent 19 times out of 20". This is saying that

was big enough so that

was big enough so that

was 95%. (This requires

was 95%. (This requires

of about 1067.)

of about 1067.)

Problems:

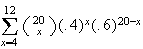

-

Tomato seeds germinate (sprout to produce a plant) independently of each

other, with probability 0.8 of each seed germinating. Give an expression for

the probability that at least 75 seeds out of 100 which are planted in soil

germinate. Evaluate this using a suitable approximation.

-

A metal parts manufacturer inspects each part produced. 60% are acceptable as

produced, 30% have to be repaired, and 10% are beyond repair and must be

scrapped. It costs the manufacturer $10 to repair a part, and $100 (in lost

labour and materials) to scrap a part. Find the approximate probability that

the total cost associated with inspecting 80 parts will exceed $1200.

Problems on Chapter 9

-

The diameters

of spherical particles produced by a machine are randomly distributed

according to a uniform distribution on [.6,1.0] (cm). Find the distribution of

of spherical particles produced by a machine are randomly distributed

according to a uniform distribution on [.6,1.0] (cm). Find the distribution of

,

the volume of a particle.

,

the volume of a particle.

-

A continuous random variable

has p.d.f.

has p.d.f.

-

-